As of this posting, I do not own Google stock ($GOOGL or $GOOG), and I don't plan to buy it - yet - and I'll explain why in this post.

Perhaps you may also feel the same as me and decide to stay on the sidelines for now with GOOGL, but even if you own the stock, I think it's worth looking at the other side of the story here on potential fundamental issues coming for the company.

Google has not been immune to the broader tech selloff in 2022, and it's gone from a high of over $150/share, to now sitting in the $90 range. If this was all driven by just broader market weakness, this would be a screaming buy - but there's more to this story which is worth covering today.

When you think of Google, there's many aspects to this business - they sell Pixel phones (hardware), they offer services like Gmail and Sheets, they have Google Cloud (GCP) - which is growing well - but there's 1 core revenue and profit driver for the company - advertising.

In the latest quarter, the advertising component accounted for $59B in revenue, which means it makes up over 2/3 of $GOOGL's overall revenue. The other components are relatively small in comparison, so for all intents and purposes, I see GOOGL as an ads company.

So that brings me to my first issue - the high concentration in 1 market.

The problem builds on itself though - because this 1 market is currently feeling the heat and will continue to compress until the economy recovers and businesses raise their marketing budgets again. Over the past decade, we had excellent economic times, and Google thrived - ads grew and the economy grew but this has now reversed in 2023.

This alone isn't a massive concern for me though, because $META is a stock I own, and it was on deep discount when it dropped under $100/share when there was extreme fear around their future. But around those prices, even with the economy contracting and the ads business contracting industry-wide, $META was a screaming buy.

I don't think $GOOGL is quite at that point - not yet.

I think we need more doom and gloom, more "Google is done" videos on YouTube and blogs, before we can truly see a capitulation in $GOOGL stock and see those deep discount levels.

One trigger that may be starting to drive early stages of capitulation is this new battle with Microsoft $MSFT.

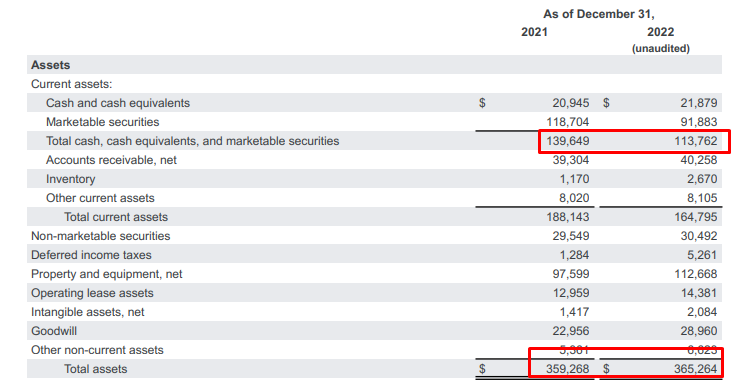

When you're a $1T company like $GOOGL is and have quite literally over $365B in assets with over $113B in CASH ready to go, there aren't many companies out there that can truly pose a threat to your business and moat.

Think about it - if you're a smaller company trying to compete with Google in some segment - Google can literally just buy them out and eliminate that threat. So there's quite literally only a handful of companies that Google CANNOT do this with - Apple, Tesla, Amazon, Meta - and of course - Microsoft.

This is significant because Microsoft now has stepped up and decided they are going to compete - and in Satya Nadella's words, they want people to know Microsoft made them dance.

Of course I'm referring to ChatGPT, and the Microsoft investment with Bing and their Edge browser. Microsoft also has deep pockets - they can afford to invest and burn cash here to capture a small portion of Google's search business which drives most of their ads, and this would hurt Google's bottom line - and in turn could result in them scaling back on investments on GCP - which BTW is a cash burn business for Google today.

This is significant because GCP competes with MSFT's cash cow - Azure. There's some 4D chess going on here, and it's super interesting to watch true competition between these tech giants.

My concern is not that Google will be displaced as #1 in search and ads - I think that's unlikely. What is very likely though is a hit to margins, a potential scale back of innovation in GCP, and a result of shrinking revenue and profits - all of which makes the stock less desirable, event at seemingly discount prices.

Simultaneously, could Google turn things around and destroy ChatGPT with their competitor? Maybe - and if anyone has the data and investment budget to back it up it's Google, but AI search is more expensive than regular Google search via text, so even if Google keeps market share, margins will likely shrink and the whole advertising model will change as well - likely for the worse.

The other thing which COULD happen as the AI chat and search battle heats up, is Apple may come after Google as well. Uh oh.

Google apparently pays Apple somewhere in the ballpark of $20B/year to be the default search on iPhones - and that's a big deal. If Microsoft (through Bing) can offer a comparable, accurate product that is on par with Google search (or even 95% as good), they could charge half the price and again, this would hurt Google - bigtime.

Alternatively, Apple could demand more from Google to remain the default search on their devices, which again, hurts Google.

Or the last scenario - Apple could release their own search product, and overnight Google would lose a massive chunk of their market and revenues.

Will this happen? I think some combination of this is likely - and that is when we may see true capitulation happen with $GOOGL stock - maybe driving this down to the $70s or $60s - at which point it could be like a $META under $100 situation.

So let's see - I'm patient with this one.

If things turn around, great, congratulations to anyone who has been buying this weakness in the stock. For me though, I don't feel strongly about owning it at this price given the risks, so I'm fine missing out if this recovers. After all, through $META I'm still exposed to the illusive ads market.

I'm curious - do you share the same concerns as me with owning $GOOGL, at these prices? Is there a different perspective that you see things at? Tweet me @thecompounderco to share your perspective.